A few weeks back, I was commenting a post by Vuk Vuković on his blog. For those who don’t know who Vuk is, you can check his blog here. As always, somehow I turned the subject to some monetary affairs, where Vuk invited me to check his post on Market Monetarism. This is the reason I’m writing this now. And for those of you wondering, why am I suddenly writing in English – it is because Vuk’s blog is in English, and I thought it would be appropriate to reply this way, in case some of his followers want to join the debate. This post was suppose to be a response (a comment) to a post Vuk did about Market Monetarism. Unfortunately, I haven’t found time to write Croatian “sum up” of what Market Monetarism is, and why is it gaining “popularity”. For those who are willing to learn more before reading this, take a look at this paper by Lars Christensen.

I have never been in a economic talk with a person with so much knowledge like Vuk. I hope he won’t be angry I’m referring to him just by his name (?). First time I found about his work, was one time I was sitting in a class listening to someone’s pretty boring presentation. Presentation was apparently also boring for the assistant who was supposed to listen to it, so he was reading a paper. I caught a glimpse of the name and the author, and found the paper on my mobile phone. I started reading. The paper vas Vuk’s “Political Economy of the US Financial Crisis 2007-2009” which I really recommend to anyone who wants to have a thorough insight on what was going on, especially prior to the start of the crisis. It really advanced my views on the matter. This year I ran into his blog on the Internet, and added it to my reading list. I encourage everyone to take a look at his blog, because his own thoughts are always accompanied by some new paper, so you can stay up to date with the latest research – I wish more bloggers would do so.

While I myself don’t yet have all the facts and ideas on how to look at the crisis and the role of monetary policy nicely “sitting” in my head, I find market monetarism quite interesting, and so far, I am convinced this is a good idea. That is the reason I decided to take up Vuk’s offer to take a look at his post and write what I think – at some point I was also wondering “how do I see all of this?”. This will help me settle my thoughts in a way, at least I hope.

You can find the original post here, I have quoted some parts of the text so it is easier to follow.

“They [market monetarists], in fact, believe that monetary stimulus is the only thing that can help the economy at this moment.”

Well, they do believe so, because they identify the cause of the “Great” Recession being the failure of the Fed (or ECB) to act when the money demand increased rapidly in the second half of the 2008. They also don’t like calling it stimulus because they would prefer it to be a natural response to the deviation in NGDP from the pre-crisis path – a path that was basically created by the Great moderation, starting about 1987, after the Volcker disinflation. It would be part of a RULES based framework that they call NGDP targeting. Stimulus, to me, sounds like discretion. Discretion is what was happening all this time. QE3 was a step in a good direction, but just a step. Fed tied it to its confusing dual mandate (which is in my view a relic of some different times of the past). Unfortunately, to my knowledge, only Congress can change Feds mandate. On the other side, regarding the fact that Fed did a mistake, even Bernanke acknowledges (or acknowledged in 2003) that inflation and NGDP are the best indicators of the stance of monetary policy, the question is, why didn’t he respond to these indicators in 2008. The reason why they believe it is the only thing, comes from the fact that money demand is elevated, not least because a lot of uncertainties hanging around the globe, so this money demand must be satisfied by Feds action. You could wait for the politicians to resolve all these things, but they havent been ready to make the right moves in the past, so why should they do it soon? This way CBs can help in stabilizing the environment, and even give an impulse to AD after acknowledging the elevated money demand is a reason to act, but again, in my view trough a rules based framework and not discretion.

“current QE efforts create money for banks that isn’t being released into the real economy. It makes perfect sense for banks to hoard cash and deposit money in central banks overnight when alternative investments over low interest rates are relatively more risky.”

Well, most market monetarists do believe that interest on reserves shouldn’t exist (as it hasn’t existed before the crisis) – it is the primary reason banks hoard reserves. Opportunity costs are non existent since T-bills are yielding the same interest. So called IROR must go. I also believe focus on banks was also one of the bottlenecks of the Feds reaction, since Fed was more preoccupied saving the primary dealers than focusing on the inflation or NGDP and the economy (and that’s not rules – that is discretion: discretion they don’t like :D). This is a point that was originally brought up by a “free banker” George Selgin who calls for reform of the way Fed conducts its OMOs – you can find the paper here. Sumner for instance would even like to see some non bank agents being counterparties in Feds operations (preferebly using NGDP futures)

“The second favorable idea is to credibly signal long term easier monetary policy, when interest rates are no longer zero. The central argument is that this signal of easier money in the future and expectations of rising demand will induce people to spend more today. This does make sense as businesses would make investments today if they would be certain that these investments would pay off in the future. It’s the uncertainty of today that’s killing off their investments and hiring. So a credible signal of monetary policy would be enough to break the uncertainty surrounding their investment decisions. “

Yes, it does make sense. MMs see NGDP as the indicator of the monetary policy stance. They believe credible signal about NGDP in the future, starting from now, would be able to improve conditions. Markets would in that scenario also do big part of the heavy lifting, without much need for large programs (remember CHF moving after the 1,20/EUR announcement without SNB moving a finger, or Euro yields after Draghi’s “magical” words). Businesses mostly don’t make investment decisions based on the actions of the central bank, and they shouldn’t, they ought to care about the relative price signals. Monetary policy should be the one that doesn’t affect relative prices. This is something where MMs and free bankers agree, and in a way a lot of MMs see NGDPLT as a possible transition to free banking. But markets do respond to monetary policy, in the US where markets are used for 75% of the financing this matters this is important, same as in Europe where the shift towards bank wholesale funding also happened during the last 15yrs – so markets do matter, and their expectations do matter. This kind of policy would also be conductive to creation of more private safe assets that are now “missing” form the system. CBs are focusing on the money market, effectively crowding out the market (ECB); or in the US where QE is tied to a counterintuitive target like lowering long term yields, or worse – tied to the real variable like the unemployment goal.

“The ‘rule of thumb’ target would be 5% (2% inflation plus 3% real GDP growth which is a potential GDP growth path). This implies that if nominal GDP falls to around 2% per year, the Fed should allow for temporary higher inflation to reach the 5% nominal growth target.”

Not all MMs believe that 5% NGDPLT is the right target, but all of them believe a target has to be set. They don’t think that we need higher inflation now in order to achieve target, because they don’t care how the target is split. But they do believe it does allow for a flexible inflation for the times where we have negative supply shocks and higher inflation/ cases of positive supply shock and lower inflation. In inflation targeting regime central bank will perceive a positive shock from the supply side (causes lower inflation) as a divergence from the target and try to hit the target by unnecessarily easing and possibly creating bubbles. I it also works the other way around, where CB will try to tame inflation by curbing already disturbed economic activity. Government, too, can be source of these shocks, and should be identified as such. If inflation is rising and RGDP falling, government is, in absence of external shocks, doing something wrong which is hurting growth – as now with obamacare, fiscal cliff uncertainty, overregulation, euro crisis uncertainty….

Even return to a pre-crisis path isn’t instrumental, adopting a new rules based policy is, it can continue on current path, without making up for what was “lost” because of previous mistakes.

“The idea can literary translate to the following: If the Fed prints more money, this drives up prices (the classical causal relation in monetary economics where more money in the economy makes it lose its value and triggers an increase in prices as people now need more currency to buy the same goods as before). Higher prices of goods and services will increase the GDP measured in current prices (nominal GDP). This is an easy way to reach the target without increasing real growth at all. For the current 1% rate of real growth the Fed may pump up inflation to 3,5% in order to reach its target. But this doesn’t mean the economy grew at 4,5% – it’s real growth is still weak.”

MMs don’t think in these terms, as I already explained. Vuk knows that prices will not rise at once, and MMs don’t think that policy will be achieving the target by raising inflation. Its not about inflation, its about demand – the idea is to create a “hot potato” effect, where public will hold more money than they want to – and spend it. If there is talk about inflation, it is a talk regarding Feds target of 2%, and Fed is failing to hit its own target as well. But they do know that current spending is strongly related to expectations of future incomes, and that’s why the credible income target is set, if possible using the futures markets to target the forecast. As I already mentioned, markets will do a big part of the heavy lifting then. Talking about real growth component makes no sense because monetary policy has no effect on long term growth and that’s why the described scenario would be only governments “fault” in absence of other shocks from outside.

“That’s why current proposals for NGDP targeting are a strictly short-run monetary stimulus that can be used to get the economy out of a recession and on to its potential output path. “

It makes no sense to take up on NGDP target now, just for the sake of stimulus, to abandon it in the future. I think Sumner as trying to indicate that he doesn’t believe in long term positive relationship between money printing and real growth. Its about resolving the problem of high money demand. (It may be a little obvious, but I was surprised how many people still believe the good ol Phillips curve is valid indefinitely). I do agree with Vuk that Reagan’s reforms meant a lot, but I think they had more to do with the credibility of the new administration and expectations about the future – meaning Volcker on one side steering the monetary policy toward lower stable inflation and a credible target plus Reagan being a president supporting him. Reagan was also doing his part of the job – freeing the economy (as Vuk wrote), after it was finally recognized by the public that all those regulations and taxes don’t help general welfare. I feel Friedman was also a major player in this, by communicating the ideas to the public the whole decade before Reagan’s election. But, you can’t expect Reagan’s kind of reforms to work their way through the economy in a year (he was president from 1981, and Vuk was talking about 1982).

( ***Its funny how history repeats itself. I think we are in a similar position now. Unfortunately we don’t have a new Friedman in ranks of the economists to drive the push toward more freedom and markets. So I guess we will have to learn the hard way again…or is this now Keynes’ second coming (in form of P. Krugman or worse, J. Stiglitz) – God I hope its not!)

Vuk basically believes this crisis is a structural one, and response to the crisis should defined by this fact:

The biggest problem I have with this approach is that it assumes that the crisis was just another aggregate demand shock which can be resolved by short-run stimuli. This perhaps was the case with the 2001 recession (which was initiated by a series of shocks like the 9/11 attacks, dot-com boom, and corporate scandals like Enron), and it may even be applicable today if the shock was being constrained on the housing market alone. But that’s not what happened. The housing market bust was just a trigger for the unsustainable system to fall. The answer cannot be to wait for businesses and consumers to continue what they’ve been doing before, the answer must be in creating and finding new jobs and new patterns of production and labour specialization.

I don’t think there has to be a difference in the view of the causes of the crisis, at least not in the question of the place where disturbances began. Everyone agrees that problems of the subprime market (which was a small part of the overall market were the start) are at the core of the problems that began in 2006. The point where I believe Vuk sees things differently than MMs is the Q3 of 2008. As I wrote, Vuk believes structural problems are responsible for most of the Great Recession, and the slow recovery.

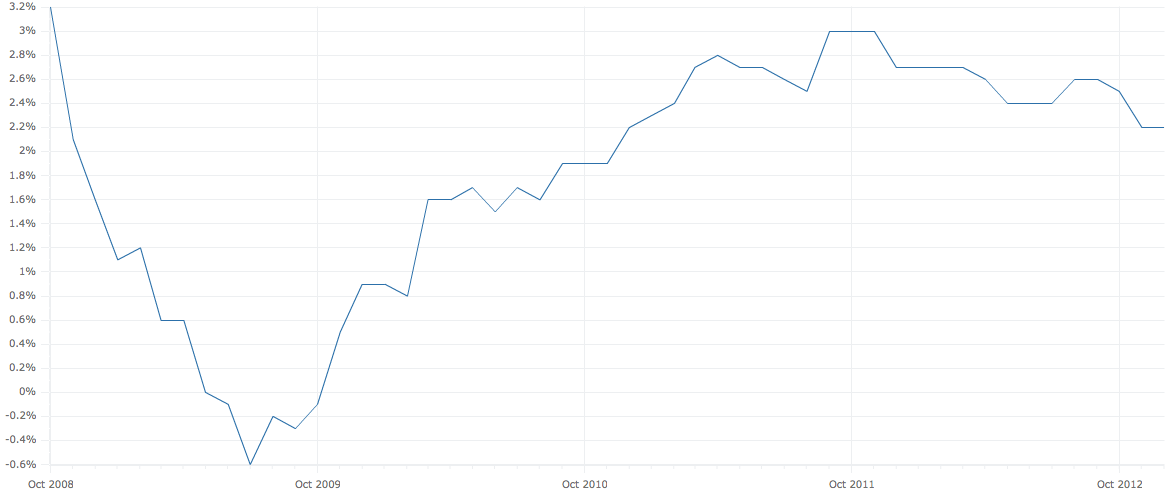

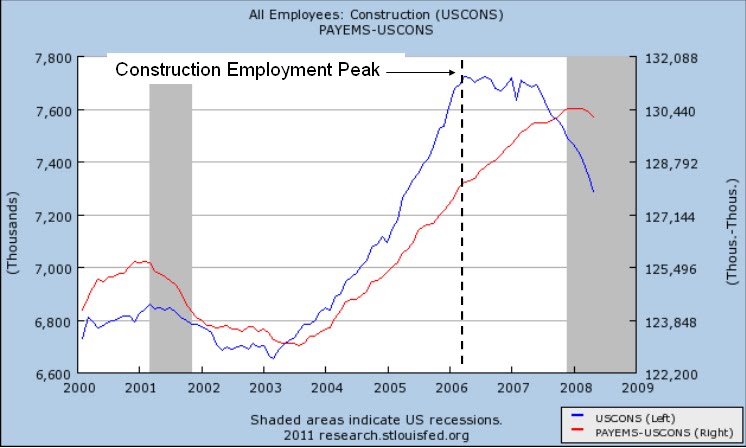

David Beckworth illustrates the other view nicely in the following graphs,

Here we see construction employment versus total employment less construction employment

You can see these graphs, along some other ones, on Beckworths blog, these posts. Beckworth has something to say about labour mismatch problem here

So we see that NGDP, as employment, was stable for more that a year after the subprime problems started surfacing. I think this shows that the reallocation between sector that were hit structurally and other sectors that needed new workers (employment kept growing) was happening in a stable environment until 2008. The adjective “great” has accompanied this recession only in the mentioned Q3 of 2008 when Fed for various reasons and policy errors failed to react to the growing money demand causing a fall in the NGDP causing the “Great” Recession.

Or how Beckworth puts it

focus on 2006-2008 period and see that the structural changes did not require a collapse in AD.

I believe this inter-sectoral “unwinding” and restructuring could have occurred in a less messy environment in case Fed was following its own inflation target and saw the breakeven inflation which tanked, as an obvious sign that money is tight. So while I do believe we have structural problems caused by our governments exstensive action in the markets, I do think the recession could have been milder if , first the Fed, and ECB, reacted because they recognized they have passively tightened the money supply causing NGDP to dip in the second half of 2008, and later 2009 which was a recession year.

“Even if we accept the claims that tight money made the recession much worse, monetary policy didn’t cause the recession. At least not single-handedly.”

I basically agree. It is Feds only job, as an monopoly issuer of currency to accommodate the demand for the reserves/currency. Fed didn’t cause the recession, but it did turn it into a “Great” Recession. Government, creating a terrible system to advance a political goal caused, bigger than usual, structural problem in economy, with repercussions to the financial sector, which would probably cause a recession, albeit a milder one than the one we are experienced (ing?).

Now I do have a “moral” problem with all of this – and it’s the one Vuk is talking about, and it is the reason why I used to think recession will be a good thing. I hoped the crash will be a push for people and the politicians to support reforms. Unfortunately, this crisis is a fault of capitalism, at least that is what most of the people believe. Radical policies that constrain freedom of individuals are enacted, which will in my opinion cause a lot of suffering.

20th century was the battle for the freedom of nations, 21st, seems to me, will be the one where we will fight for the freedom of the individual.

I obviusly still have a lot to learn from writing of people like the late professor Buchanan.

That’s why I was, in a way, a proponent of the German push for reforms in the Europe periphery, and against any easing by the ECB. I saw it as mimicking Bundesbank’s orthodoxy and resistance to help politicians in any way, so the only thing that was left for them to do was reform. I admit, I never thought there would be this much resistance. I think public in most countries isn’t grasping the reality that currently they don’t have any other option.

In the comments Vuk did write he doesn’t believe Fed can start necessary restructuring. And I agree. But Fed can create environment where such restructuring will be easier to carry out. It is important that Fed adopts a rules based policy that will not distort relative prices, unlike current discretionary measures that are altered every year. I think Vuk would also agree that restructuring in the Euro Area periphery is easier now when Draghi assured markets that he will do “everything necessary”. So the outlook is more stable and policy makers can concentrate on doing the reforms. The period before that was just awful. We had urgency meetings of the Euro club countries every now and then, because different measures they were proposing, together with some irresponsible economists calling the end of euro, were roiling the markets. Policymakers focused on the markets instead of focusing on reforms. That was noticed in the public, which, again, blamed “capitalism”, bankers, Angela Merkel for all their misery. Now environment is much friendlier to talk about the ways Euro area, and the EU can improve their institutional setting. How responsible would it be if Cameron held his EU speech a year ago? Here I must say that I do agree with Jens Weidmann, who is worried about the effects various rescue funds will have for the future of the Euro, since they do create “uncomfortable” feeling of additional moral hazard in the system. And when you compare effects Draghis words had on the markets, after so much taxpayer money thrown into these funds and different bailouts, one can see why a good monetary policy is not the panacea, but it can offer a helping hand. With more CB guidance/activity markets will lend a hand too.

Bottom line: Don’t observe the idea of NGDPLT targeting and its effects form a perspective of temporary stimulus, even in this economy.

New target doesnt have to mean going back to pre crisis level and continuing the precrsis path. A new one can be started from this point.

Monetary policy can’t fix structural problems but it can create environment where the whole thing doesn’t have to be messy as now.

UPDATE: I just found a interesting response by Lars Christensen to George Selgin, on similar questions as Vuk’s so take a look. There, you can find links to the responses of some others of the market monetarist bunch, as well as some recommended posts on the topic.

+Heres Sumner and Beckworth discussing some of the basics about NGDPLT. Too bad, there weren’t more questions at the end.