Kolega s bloga Strašilo ima post koji povezuje nisku kamatnu stopu i inflaciju u Hrvatskoj. To je relativno konvencionalno razmišljanje o samoj inflaciji kao monetarnom fenomenu i cilju modernih središnjih banaka, kao i dosezanja istog cilja ciljanjem kamatnih stopa. Evo par mojih misli na tu temu.

Milton Friedman je prije nego što smo svi postali “osviješteni” nakon 80ih izjavio “Inflacija je uvijek i svugdje monetarni fenomen”. Pitanje je koja inflacija? Povećanje cijena zbog promjena u strani ponude možda ne bi smjeli zvati inflacija, ali greška modernih središnjih banaka je da se fokusiraju na takve promjene ciljajući nekakvu košaru u formi CPI-a. Tako sada o inflaciji pričamo u slučaju inflacije monetarne mase i npr. rastu cijena koji je pruzročen tsunamijem.

Činjenica je da su određene komponente više pridonijele rastu indeksa cijena u Hrvatskoj od drugih. Prije svega to je pitanje cijena energije. Početkom 2012. značajno je podignuta cijena električne energije, jednostavnom administrativnom odlukom vlade. To je povećalo pritisak na inflaciju (CPI) u Hrvatskoj, kao što pokazuje HNB-ov bilten.

Tu se i kolega slaže. Quotati ću njegov komentar da otprilike vidite o čemu se radi.

OK, istina je da ne baš sama opća razina cijena, ali sam indeks može porasti i iz razloga državne odluke

ali ja tu odmah vidim nekoliko problema, konkretno, najlakše je ustvrdit nešto tipa, da, ali par godina prije nisu podizane cijene kada su trebale bit već je državna firma snosila dio troška inflacije i sada su cijene na onoj razini na kojoj bi ionako trebale bit

činjenica je da opća razina cijena divlja, i iako tržište novca u hrvatskoj nije nešto razvijeno, ipak bar u velikoj mjeri prikazuje rezultate monetarne politike i koliko ima “viška”/”manjka na tržištu”

tu sam još davno htio pisat o tom HNB-ovom cilju, jer oni imaju zakonsku obvezu održavat stabilnost cijena, a inflacija od 4% nije stabilnost cijena

da stvar bude gora, ta zakonska obveza je tu da bi bili usklađeni s ECB, a tamo je to (ili je bar bilo prije par godina 2%)

siguran sam da imaju neku uredbu ili što već na temelju čega je to savršeno legalno, no ostaje činjenica da krše minimalno duh zakona na temelju kojega postoje

Njegov komentar u biti i predstavlja strukturu nastavka teksta – pitanje izvora inflacije, kamatnih stopa kao instrumenta monetarne politike i pitanja zakonskog reguliranja cilja monetarne politike.

U principu ima pravo sto se tice “tajminga”, postojao je negdje u publikacijama HNB-a graf tih cijena gdje se jasno vidjela razlika između Hrvatske i EU zemalja (ako netko nađe neka linka, hvala). Dio rasta cijena je naravno monetarna strana (na globalnom nivu) ali ni blizu sve. Na primjeru HEP-a – naglim povećanjem cijena akomodirana je neefikasnost državne firme i troškovi su preneseni na kupce (doduše dio su i globalni supply side faktori). Jednako tako, rastom stope PDV-a akomodirana je neefikasnost države u pružanju svih usluga – plaćamo više za isto. To je nešto na što monetarna politika ne može utjecati, nit bi smjela pokušavati. Ono na što je želim staviti težište u ovom postu nije samo pitanje uzroka inflacije, već pitanja odnosa monetarne politike koja cilja inflaciju i samog cilja – inflacije.

Stabilnost cijena ne podrazumjeva samo promjene stope trenda kroz vrijeme. Kada pričamo o stabilnosti cijena, ekonomisti obično podrazumjevaju i manju volatilnost cijena. Recimo, Velika moderacija nije period (samo) niske inflacije vec stabilne inflacije (kao i outputa) u smislu volatilnosti. Ima mnogo razloga zasto je 2% “optimalna” inflacija, no to je relativno nov fenomen, više-manje povezan s Greenspanovom erom – tek je Bernanke artikulirao 2% kao cilj. Eurozona ima cilj od “manje ali blizu” 2%.

Ako preferiramo “austrij(an)ski” stav o inflaciji u smislu gubitka vrijednosti valute – prebacimo se u nekakav “productivity norm” svijet. Tu je bilo koji nivo monetarne inflacije nepoželjan. Tada je, pojednostavljeno, (ciljana) inflacija (demand side – uzrokovana povećanjem monetarne mase u odnosu na potražnju) efektivno 0, a ekonomija je u deflaciji koja je rezultat povećanja produktivnosti (supply side). Deflacija bi bila jednaka rastu produktivnosti. Čak i u tom svijetu, pad efikasnosti monopolističkog agenta dovodi do povećanja (u biti smanjenja, ali zamislimo deflaciju kao trend ispod 0) stope deflacije, tj percepcije rastućih cijena (cijelog indeksa) u odnosu na prije. Kao što sam rekao, to je nešto na što središnje banke ne bi trebale reagirati jer je velika vjerojatnost da će imati negativne efekte na alokaciju, a makro efekti će i u kratkom roku biti nepovoljni. Ako pogledamo rezultat Bernankeovog ciljanja inflacije 2008. možemo reći da su efekti već i dugoročni. U lice s povećanjem cijena koje je rezultat negativnog šoka ponude (i negativnog utjecaja na realni rast), monetarna politika koja cilja inflaciju će pokušavati smanjiti domaću aktivnost, koja je već pod negativnim utjecajem negativnog supply šoka.

Hrvatska, kad/ako uđe u eurozonu, dolazi pod palicu ECB-a kojemu je cilj, kako kolega navodi, 2%. To je naravno mjera HICP-a za cijelu eurozonu. Možda će u Hrvatskoj inflacija mjerena HICP-om i nakon toga biti 3-4%. To naravno nije razlog da ne preferiramo inflaciju od 2%, onoj od 4%. Ostaje pitanje kako je mjeriti i kako ostvariti cilj, te kako to zakonski regulirati. Lars Christensen ima ideju kako ostvariti cilj.

Kamatne stope nisu stav monetarne politike

S obzirom da sam do posta došao jer sam kliknuo na Friedman tag na blogu, možda bi bilo dobro iskoristiti njegove riječi za ilustraciju cinjenice da kamatna stopa nije dobar pokazatelj stava monetarne politike:

Low interest rates are generally a sign that money has been tight, as in Japan; high interest rates, that money has been easy.

. . .

After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high interest rates and easy money with low interest rates was dead. Apparently, old fallacies never die.

Problem je što većina ljudi kamatne stope gleda kao nešto čime se bavi središnja banka, a ne kao tržišni fenomen. Oni koji to razume – zarađuju, tako je Goldmanov Lloyd Blankfein u Davosu izjavio kako će kamatne stope narasti onda kada tržište to kaže.

Niske kamatne stope

ne moraju biti znak nadolazeće inflacije. Upravo iz razloga koje sam naveo prije, tj na primjeru Hrvatske, gdje kamatni kanal u principu i ne postoji, pa kad se i spuste stope na tržištu novca, to ne stvara nikakav efekt na cijenu kredita s obzirom da je ona zadana na drugi način. Nije stvar nerazvijenosti tržišta, vec činjenice da HNB

uvozi monetarnu politiku ECB-a tako što drži tečaj “stabilnim”.

Naprotiv, upravo su visoke kamatne stope (c.p.) inflacionarne jer povećavaju brzinu obrtaja novca.

Kamatne stope su relativno “nov” način provođenja monetarne politike, a posljednjih 20 godina posebno povezan s formulacijom

Taylor rulea. Fokus na kamatnu stopu je u biti rezultat keynesijanskog prodiranja u mainstream ekonomiju krajem 80ih. Nakon financijskih inovacija 80ih volatilnost obrataja novca (money velocity) je uvjetovala neuspjeh Friedmanove ideje da se cilja M2 novčani agregat. S druge strane serija znanstvenih radova u SAD-u je pokazala da monetarni agregati gube vezu s realnim varijablama dok kamatne stope utječu na realne varijable. Danas znamo da to nije istina i da je ovaj način razmišljanja rezultat lošeg mjerenja monetarne baze. Ireland i Belongia to

pokazuju to koristeći nove DIVISIA monetarne agregate. Hoću reći da je fokus na kamatne stope zapravo rezultat lošeg mjerenja agregata više nego uspjeh monetarne politike vođene ciljanjem kamatnih stopa.

Kamatne stope, kao i tečaj su rezultat upravljanja monetarnom bazom. S obzirom da je monetarna baza loš instrument za ciljanje , Woolfordova

biblija je skupa sa popularizacijom Taylor rulea kao izvora Velike moderacije, kamate uvela u priču o središnjim bankama. Zašto po meni to nema smisla djelomično sam odgovorio, a povezano je i s činjenicom da se središnja banka zapravo ne bi uopće trebala povezivati sa bankama a o tome više drugi put.

Stav monetarne politike predstavljaju NGDP i inflacija, a ne kamatne stope. Da se kratko vratimo na Hrvatsku – dok kolega smatra da je rastuća inflacija rezultat HNB-ove ekspanzivne poltiike, ja se ne slažem. Quotati ću vlastiti komentar:

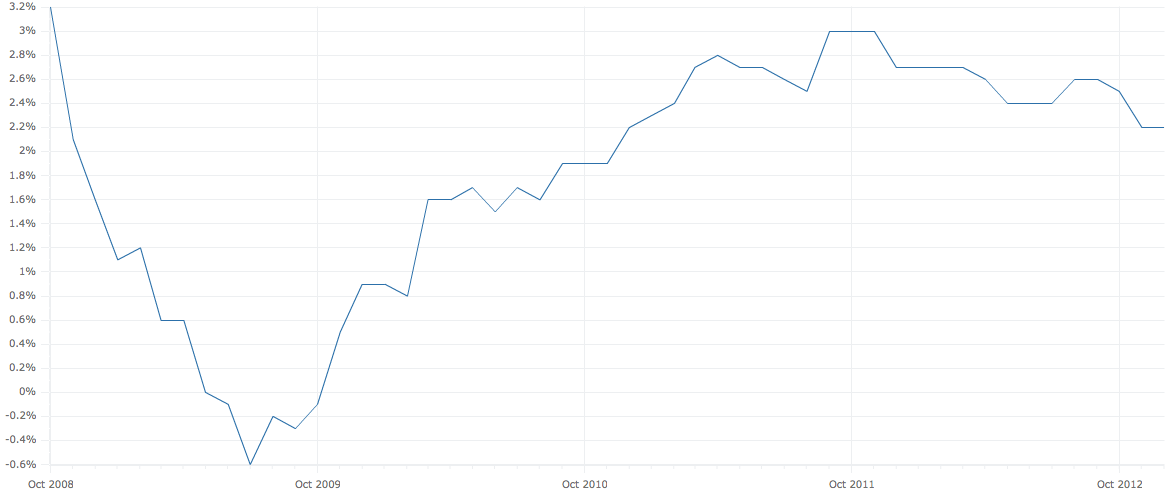

Inflacija u 2012 u RH je prije svega supply side, tj negativni supply sok koji je proizvela drzava intervencijama u porezni sustav i nagle promjene cijena koje kontroliraju drzavna poduzeca (poput el.energije). Na takve sokove sredisnje banke ne bi smjele reagirati jer sredisnja banka po svojoj definiciji ne moze ni utjecati na supply side faktore. To je nesto s cime bi se slozili i free bankeri poput Georgea Selgina. Kad bi pretpostavili da HNB ima definiran cilj za inflaciju (do 2008 oko 4%), ispunjenje istog bi najbolj pokazao GDP deflator (jer obuhvaca sve cijene a ne kosaru) vidjeli bi da je HNB profulao cilj. evo nekakav prikaz kako to izgleda

Iz moje perspektive, monetarna politika u Hrvatskoj nije ekspanzivna već suprotno.

No, konkretno gledajući, tu će već doći do prijepora izmedju monetaristickog i austrijanskog vidjenja situacije, a to je već tema za šire rasprave kojih ima dovoljno po netu.

Što se tiče samog reguliranja stabilnosti cijena, kao zakonski definiranog cilja monetarne politike – kao što sam već napisao, nije cak većinska važnost ostvarenja cilja na nekoj stopi (ukoliko ista nije eksplicitno definirana). SAD imaju stabilnost cijena kao jedan od ciljeva vec desetljecima, a 2% usidrene inflacije je fenomen koji se povezuje s Greenspanom i ranim 90ima. Zlatni standard je osigurao istu kupovnu moć više stoljeća, no to ne mijenja činjenicu da su cijene bile jako nestabilne. Zakon ne definira kvantitativno što je stabilnost cijena (kao ni punu zaposlenost, ako pričamo o SAD-u) Jedan od razloga je što, za početak postoji veći broj mjera inflacije. Dok Fed fokus drži na PCE indeksu (koji opet ima više verzija), u novinama se često navodi i CPI, a može se koristiti i BDP deflator itd. Već sam objasnio zašto smatram da je BDP deflator među boljim indikatorima – činjenica je da obuhvaća sve cijene finalnih dobara i usluga proizvedenih u zemlji, a to je puno bliže nečemu što monetarna politika može utjecati.

CPI ima i problem da su ponderi utjecaja pojedinih komponenti statični kroz vrijeme dok se struktura potrošnje uvijek mijenja. O prihvatljivoj volatilnost ciljanog indeksa bi bilo i suludo špekulirati.

Monetarna politika temeljena na pravilima a ne diskreciji

Vratimo se na zakonski okvir – ja sam u komentaru izrazio da problem dolazi iz činjenice da nezavisnost središnje banke omogućava širok prostor svakakvim interpretacijama kako ciljeva tako i pitanja provođenja monetarne politike. Diskrecija u vođenju monetarne politike koja se odvija zadnjih 5-6 godina je zastrašujuća. Kako bi se s zakonske strane regulirao rad središnje banke nije bitno zajamčiti neovisnost već kvalitetnu strategiju monetarne politike – provođenu pravilima (rules based), inkorporirati u neku vrstu

monetarnog ustava i monetarne politike provođene pravilima. Kao što kaže Lars Christensen,

We want central banks to stop the ad hoc’ism. In fact we don’t even like independent central banks – as we don’t want to give them the opportunity to mess up things. Instead we basically want as Milton Friedman suggested to replace the central bank with a “computer”. The computer being a clear monetary policy rule. A monetary constitution if you like.

The problem with today’s monetary policy debate is that it is not a Buchanan inspired debate, but a debate about easier or tighter monetary policy. The debate should instead be about rules versus discretions and about what rules we should have.